Tune hyperparameters of an Echo State Network (ESN) based on

time series cross-validation (i.e., rolling forecast). The input series is

split into n_split expanding-window train/test sets with test size

n_ahead. For each split and each hyperparameter combination

(alpha, rho, tau) an ESN is trained via train_esn() and

forecasts are generated via forecast_esn().

Arguments

- y

Numeric vector containing the response variable (no missing values).

- n_ahead

Integer value. The number of periods for forecasting (i.e. forecast horizon).

- n_split

Integer value. The number of rolling train/test splits.

- alpha

Numeric vector of candidate leakage rates. Smaller values produce slower reservoir state updates; larger values make the reservoir react more strongly to recent inputs.

- rho

Numeric vector of candidate spectral radii. This parameter scales the recurrent reservoir weights and affects reservoir memory and stability.

- tau

Numeric vector of candidate reservoir scaling values. Used to determine the reservoir size when

n_states = NULLintrain_esn().- min_train

Integer value. Minimum training sample size for the first split.

- ...

Further arguments passed to

train_esn()(exceptalpha,rho, andtau, which are set by the tuning grid).

Value

An object of class "tune_esn" (a list) with:

pars: Atibblewith one row per hyperparameter combination and split. Columns includealpha,rho,tau,split,train_start,train_end,test_start,test_end,mse,mae, andid.fcst: A numeric matrix of point forecasts withnrow(fcst) == nrow(pars)andncol(fcst) == n_ahead.actual: The original input seriesy(numeric vector), returned for convenience.

Details

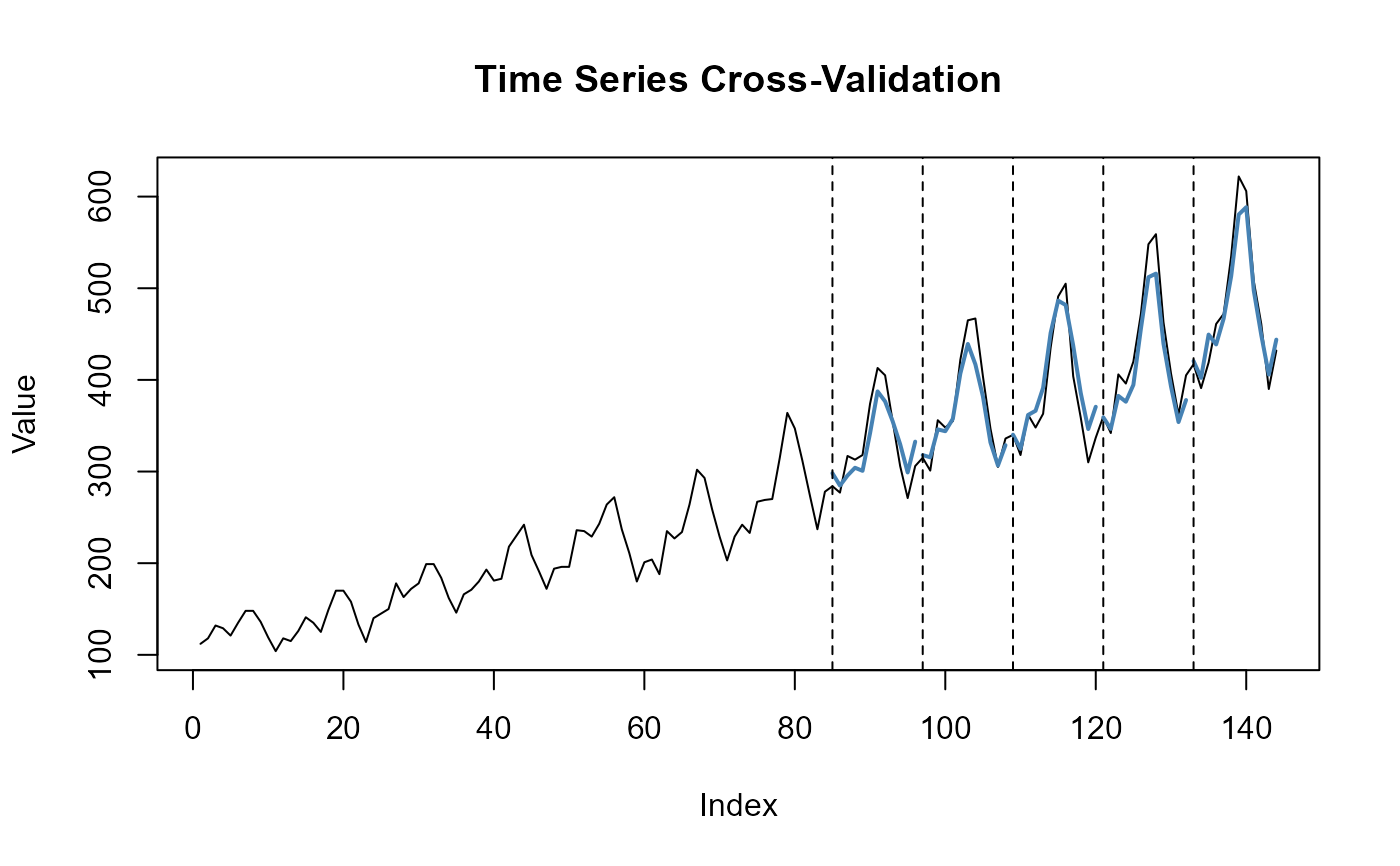

tune_esn() performs grid-based hyperparameter tuning using

expanding-window time series cross-validation. The tuning grid is formed

from all combinations of alpha, rho, and tau.

For each split, the model is trained on observations from the beginning

of the series up to the split-specific training endpoint and evaluated on

the following n_ahead observations.

For every candidate configuration and split, train_esn() is called

with the corresponding alpha, rho, and tau; all other

arguments supplied through ... are passed to train_esn().

Forecasts are generated with forecast_esn(), and the mean squared

error (mse) and mean absolute error (mae) are stored. The

accompanying summary() and plot() methods use these stored

errors to identify and display the best-performing hyperparameter

configuration.

Runtime increases approximately linearly with the number of grid combinations and the number of validation splits. Users should start with coarse grids and increase the grid resolution only where needed.

References

Häußer, A. (2026). Echo State Networks for Time Series Forecasting: Hyperparameter Sweep and Benchmarking. arXiv preprint arXiv:2602.03912, 2026. https://arxiv.org/abs/2602.03912

Jaeger, H. (2001). The “echo state” approach to analysing and training recurrent neural networks with an erratum note. Bonn, Germany: German National Research Center for Information Technology GMD Technical Report, 148(34):13.

Jaeger, H. (2002). Tutorial on training recurrent neural networks, covering BPPT, RTRL, EKF and the "echo state network" approach.

Lukosevicius, M. (2012). A practical guide to applying echo state networks. In Neural Networks: Tricks of the Trade: Second Edition, pages 659–686. Springer.

Lukosevicius, M. and Jaeger, H. (2009). Reservoir computing approaches to recurrent neural network training. Computer Science Review, 3(3):127–149.

See also

Other base functions:

forecast_esn(),

is.esn(),

is.forecast_esn(),

is.tune_esn(),

plot.esn(),

plot.forecast_esn(),

plot.tune_esn(),

print.esn(),

summary.esn(),

summary.tune_esn(),

train_esn()

Examples

xdata <- as.numeric(AirPassengers)

fit <- tune_esn(

y = xdata,

n_ahead = 12,

n_split = 5,

alpha = c(0.5, 1),

rho = c(1.0),

tau = c(0.4),

inf_crit = "bic"

)

summary(fit)

#> # A tibble: 5 × 11

#> alpha rho tau split train_start train_end test_start test_end mse mae

#> <dbl> <dbl> <dbl> <int> <int> <int> <int> <int> <dbl> <dbl>

#> 1 1 1 0.4 1 1 84 85 96 471. 19.5

#> 2 1 1 0.4 2 1 96 97 108 376. 14.2

#> 3 1 1 0.4 3 1 108 109 120 526. 19.0

#> 4 1 1 0.4 4 1 120 121 132 547. 20.2

#> 5 1 1 0.4 5 1 132 133 144 396. 17.0

#> # ℹ 1 more variable: id <int>

plot(fit)