Visualization of time series data

Alexander Häußer

Juli 2026

Source:vignettes/vignette_03_data_visualization.Rmd

vignette_03_data_visualization.RmdThe package tscv provides a set of helper functions for

time series analysis, forecasting and time series cross-validation. In

addition to functions for splitting data and evaluating forecasts, the

package contains several visualization functions that

are useful for exploratory data analysis.

This vignette demonstrates selected plotting functions from

tscv using hourly day-ahead electricity spot prices.

Installation

You can install the stable version from CRAN:

install.packages("tscv")You can install the development version from GitHub:

# install.packages("devtools")

devtools::install_github("ahaeusser/tscv")Data preparation

The data set elec_price is a tibble with

day-ahead electricity spot prices in [EUR/MWh] from the ENTSO-E

Transparency Platform. The data set contains hourly time series data

from 2019-01-01 to 2020-12-31 for eight European bidding zones.

In this vignette, we use four bidding zones:

-

DE: Germany, including Luxembourg -

FR: France -

NO1: Norway 1, Oslo -

SE1: Sweden 1, Lulea

The visualization functions in tscv work with data in

long format. Therefore, we define a context object that

identifies the relevant columns:

-

series_id: column identifying the individual time series -

value_id: column containing the numeric measurement variable -

index_id: column containing the time index

series_id = "bidding_zone"

value_id = "value"

index_id = "time"

context <- list(

series_id = series_id,

value_id = value_id,

index_id = index_id

)

# Prepare data set

main_frame <- elec_price %>%

filter(bidding_zone %in% c("DE", "FR", "NO1", "SE1"))

main_frame

#> # A tibble: 70,176 × 5

#> time item unit bidding_zone value

#> <dttm> <chr> <chr> <chr> <dbl>

#> 1 2019-01-01 00:00:00 Day-ahead Price [EUR/MWh] DE 10.1

#> 2 2019-01-01 01:00:00 Day-ahead Price [EUR/MWh] DE -4.08

#> 3 2019-01-01 02:00:00 Day-ahead Price [EUR/MWh] DE -9.91

#> 4 2019-01-01 03:00:00 Day-ahead Price [EUR/MWh] DE -7.41

#> 5 2019-01-01 04:00:00 Day-ahead Price [EUR/MWh] DE -12.6

#> 6 2019-01-01 05:00:00 Day-ahead Price [EUR/MWh] DE -17.2

#> 7 2019-01-01 06:00:00 Day-ahead Price [EUR/MWh] DE -15.1

#> 8 2019-01-01 07:00:00 Day-ahead Price [EUR/MWh] DE -4.93

#> 9 2019-01-01 08:00:00 Day-ahead Price [EUR/MWh] DE -6.33

#> 10 2019-01-01 09:00:00 Day-ahead Price [EUR/MWh] DE -4.93

#> # ℹ 70,166 more rowsLine charts

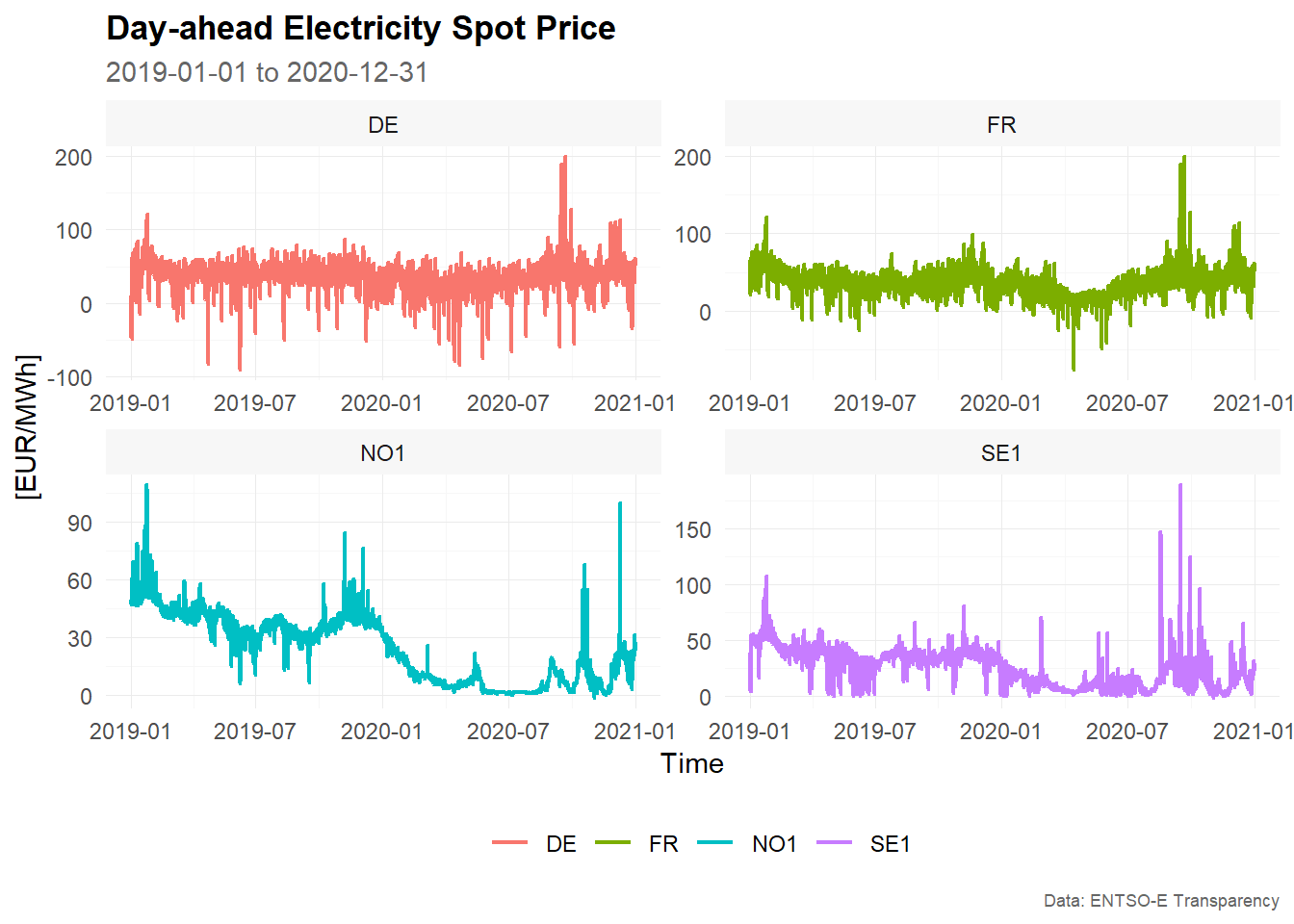

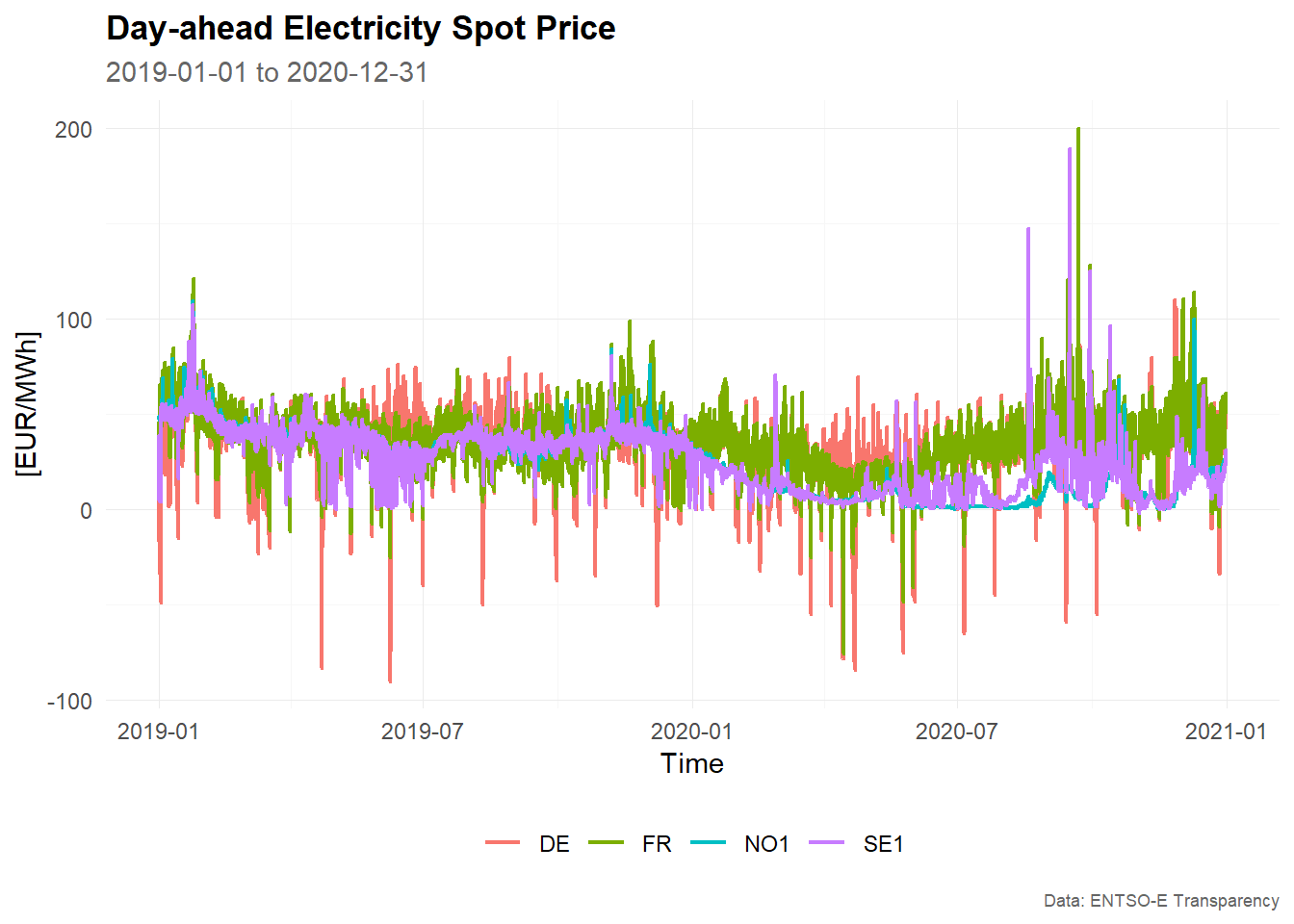

Line charts are the most common visualization for time series data. They show how the observed values change over time and are useful for detecting trends, seasonal patterns, level shifts, outliers and periods of high volatility.

The function plot_line() creates line charts from data

in long format. The first example creates a faceted plot, with one panel

for each bidding zone.

# Example 1 -------------------------------------------------------------------

main_frame %>%

plot_line(

x = time,

y = value,

color = bidding_zone,

facet_var = bidding_zone,

title = "Day-ahead Electricity Spot Price",

subtitle = "2019-01-01 to 2020-12-31",

xlab = "Time",

ylab = "[EUR/MWh]",

caption = "Data: ENTSO-E Transparency"

)

# Example 2 -------------------------------------------------------------------

main_frame %>%

plot_line(

x = time,

y = value,

color = bidding_zone,

title = "Day-ahead Electricity Spot Price",

subtitle = "2019-01-01 to 2020-12-31",

xlab = "Time",

ylab = "[EUR/MWh]",

caption = "Data: ENTSO-E Transparency"

)

The faceted version is useful when the individual time series have different levels or volatility. The combined version is useful for comparing the bidding zones directly in a single panel.

Bar charts

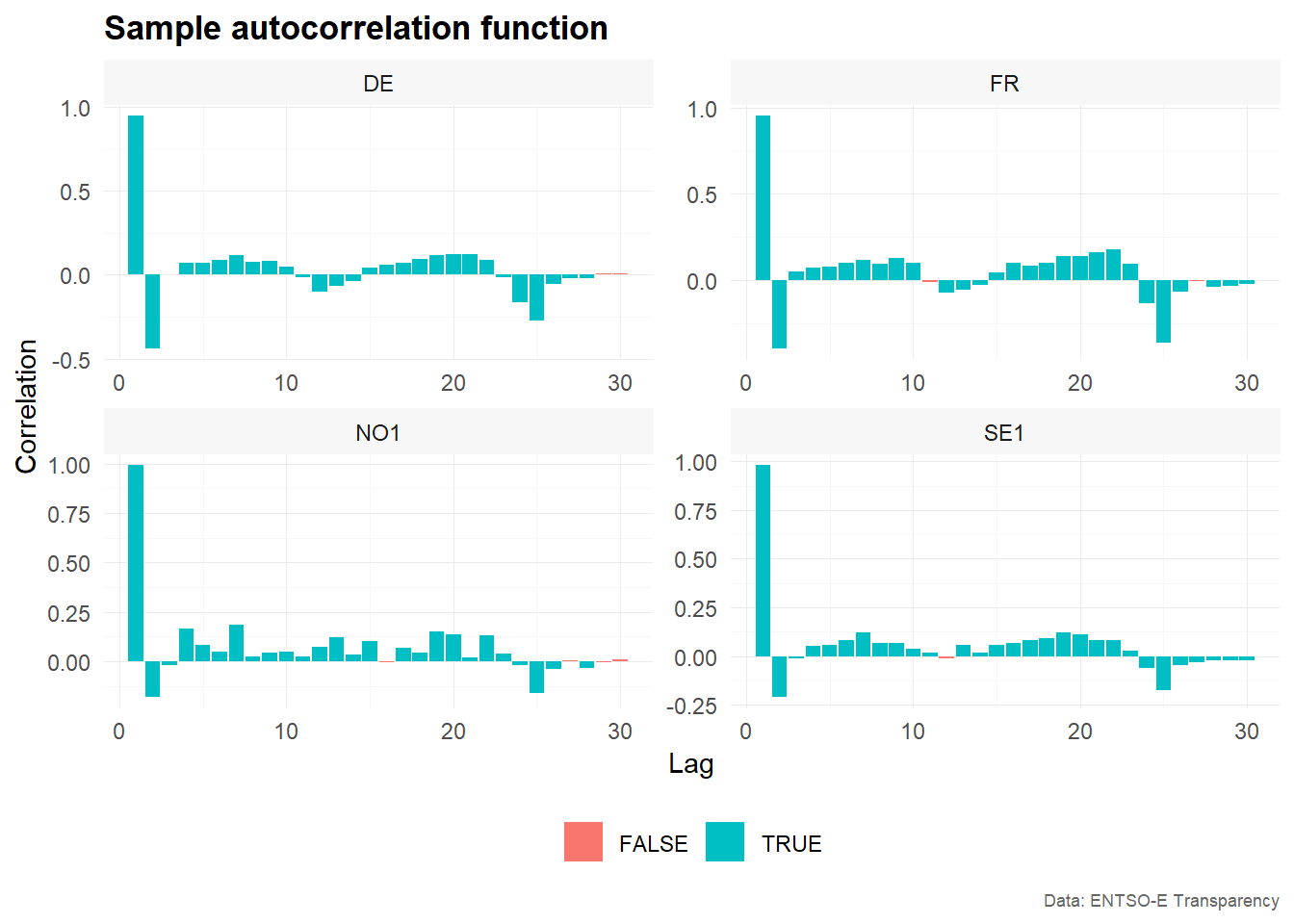

Bar charts can be used to display summary values by category or lag.

In this example, we use plot_bar() to visualize the sample

partial autocorrelation function.

The partial autocorrelation function measures the relationship between a time series and its lagged values after controlling for the intermediate lags. It is often used as an exploratory tool to identify relevant lag structures in time series models.

First, we estimate the sample partial autocorrelation function using

estimate_pacf(). The argument lag_max = 30

computes the partial autocorrelation for lags 1 to 30.

# Estimate sample partial autocorrelation function

corr_pacf <- estimate_pacf(

.data = main_frame,

context = context,

lag_max = 30

)

corr_pacf

#> # A tibble: 120 × 6

#> bidding_zone type lag value bound sign

#> <chr> <chr> <int> <dbl> <dbl> <lgl>

#> 1 DE PACF 1 0.948 0.0124 TRUE

#> 2 DE PACF 2 -0.437 0.0124 TRUE

#> 3 DE PACF 3 0.00539 0.0124 FALSE

#> 4 DE PACF 4 0.0735 0.0124 TRUE

#> 5 DE PACF 5 0.0735 0.0124 TRUE

#> 6 DE PACF 6 0.0898 0.0124 TRUE

#> 7 DE PACF 7 0.119 0.0124 TRUE

#> 8 DE PACF 8 0.0786 0.0124 TRUE

#> 9 DE PACF 9 0.0820 0.0124 TRUE

#> 10 DE PACF 10 0.0469 0.0124 TRUE

#> # ℹ 110 more rows

# Visualize PACF as correlogram

corr_pacf %>%

plot_bar(

x = lag,

y = value,

color = sign,

facet_var = bidding_zone,

position = "dodge",

title = "Sample autocorrelation function",

xlab = "Lag",

ylab = "Correlation",

caption = "Data: ENTSO-E Transparency"

)

The resulting correlogram shows the estimated partial autocorrelation

by lag and bidding zone. The variable sign indicates

whether the absolute value of the estimated partial autocorrelation

exceeds the approximate confidence bound used by

estimate_pacf().

Distributions

Distribution plots are useful for understanding the marginal distribution of the observed values. For electricity prices, this is particularly relevant because prices may show skewness, heavy tails, negative values or extreme spikes.

The following examples use histograms, density plots and QQ-plots to explore the distribution of hourly electricity prices across bidding zones.

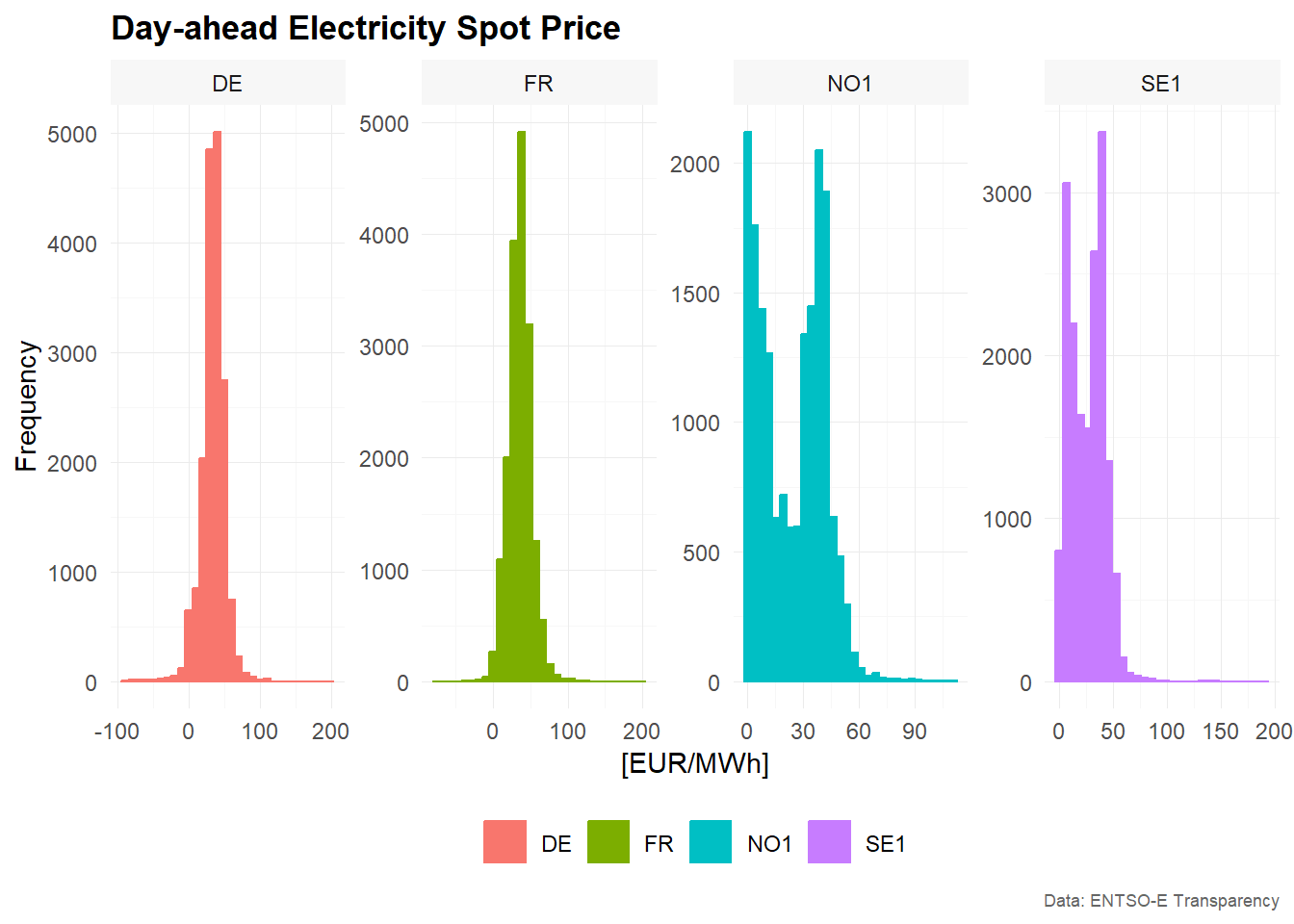

Histograms

Histograms show the frequency distribution of the observed values. They are useful for identifying the range, central tendency, skewness and outliers of a time series.

The first example overlays the distributions of the four bidding zones in one plot.

# Example 1 -------------------------------------------------------------------

main_frame %>%

plot_histogram(

x = value,

color = bidding_zone,

title = "Day-ahead Electricity Spot Price",

xlab = "[EUR/MWh]",

ylab = "Frequency",

caption = "Data: ENTSO-E Transparency"

)

#> `stat_bin()` using `bins = 30`. Pick better value `binwidth`.

# Example 2 -------------------------------------------------------------------

main_frame %>%

plot_histogram(

x = value,

color = bidding_zone,

facet_var = bidding_zone,

facet_nrow = 1,

title = "Day-ahead Electricity Spot Price",

xlab = "[EUR/MWh]",

ylab = "Frequency",

caption = "Data: ENTSO-E Transparency"

)

#> `stat_bin()` using `bins = 30`. Pick better value `binwidth`.

The faceted histogram separates the bidding zones into individual panels. This makes it easier to inspect the distribution of each time series separately, especially when the distributions overlap in the combined plot.

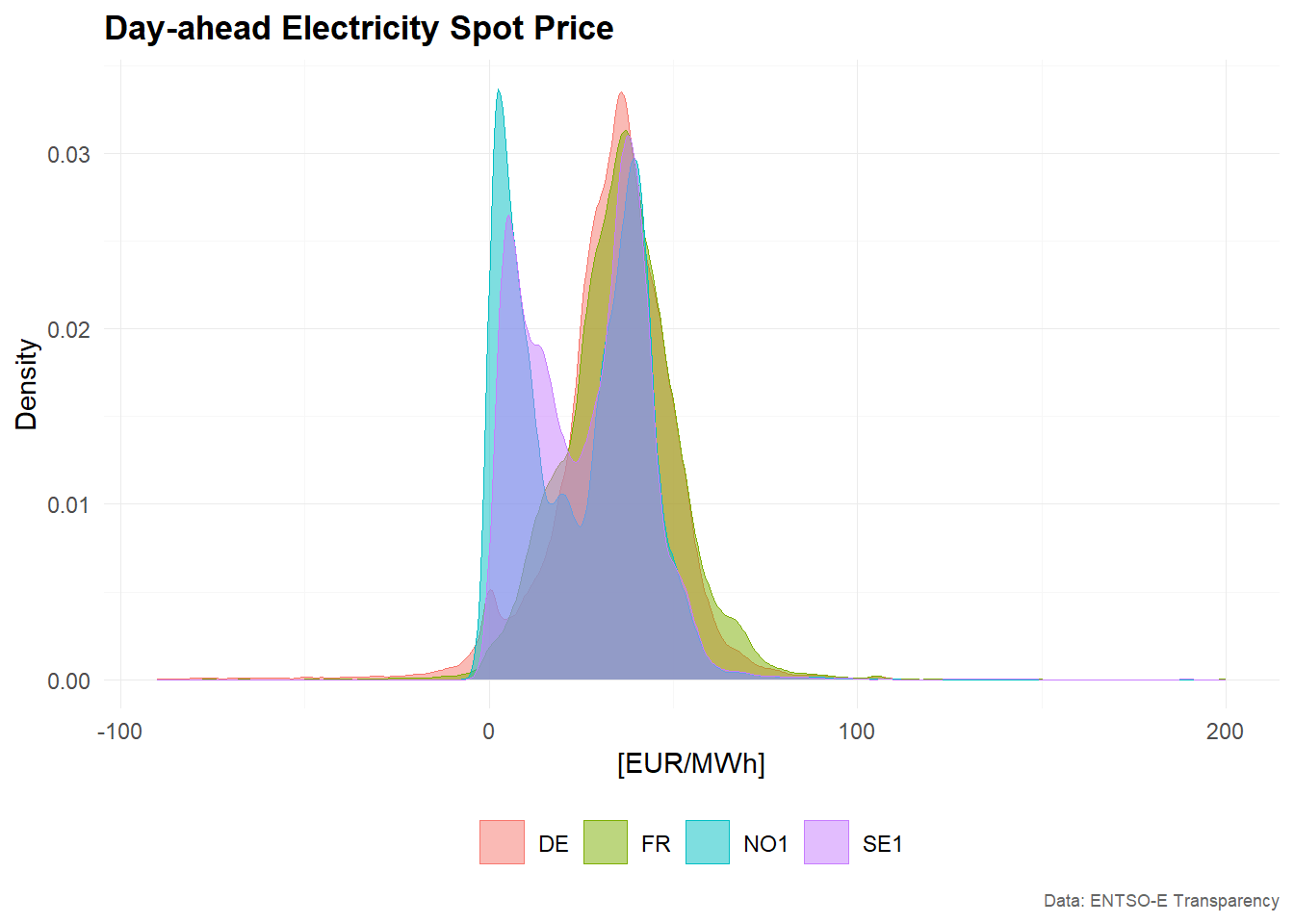

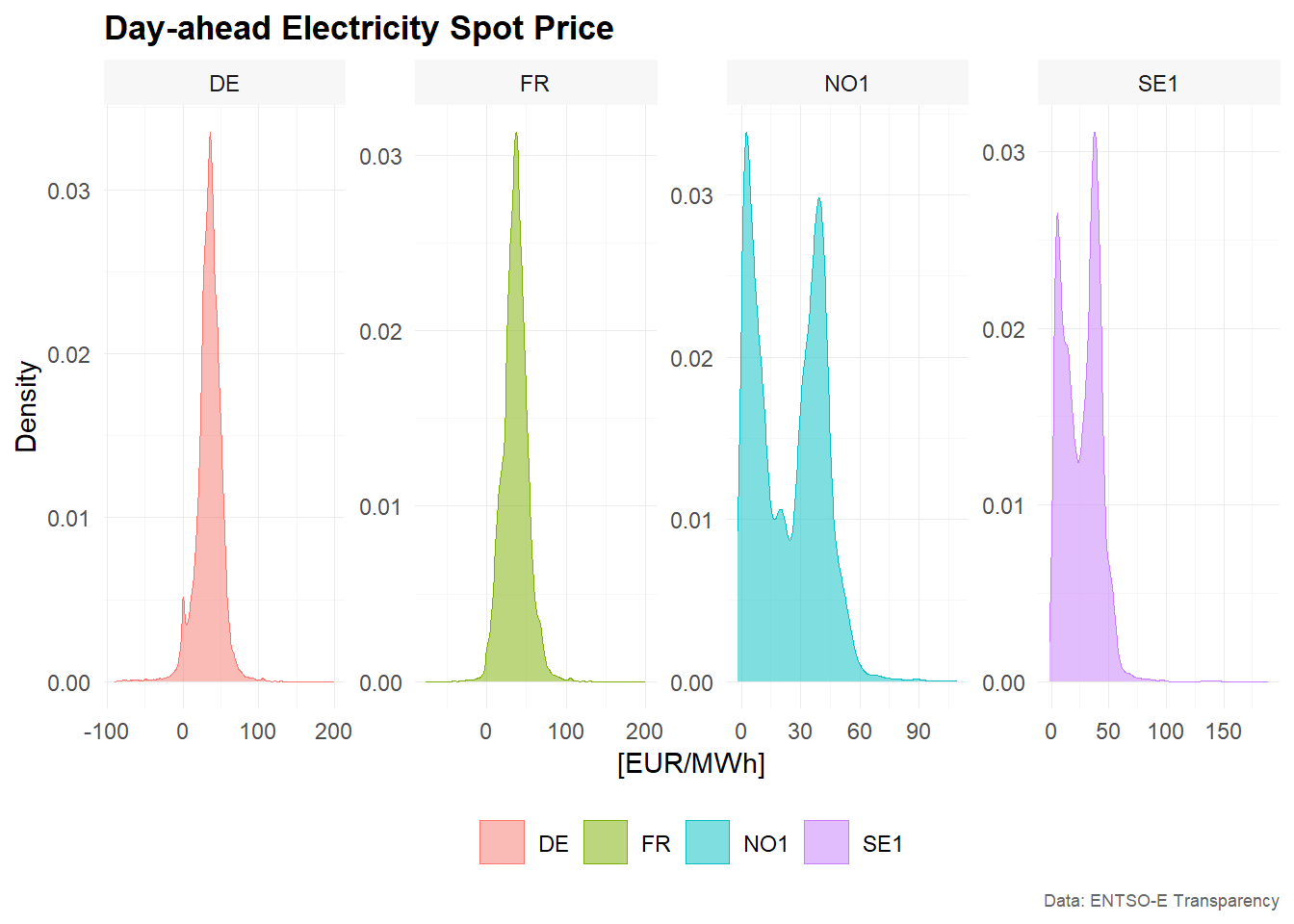

Density

Density plots provide a smoothed version of the empirical distribution. Compared with histograms, they are often easier to use when comparing several distributions in one figure.

# Example 1 -------------------------------------------------------------------

main_frame %>%

plot_density(

x = value,

color = bidding_zone,

title = "Day-ahead Electricity Spot Price",

xlab = "[EUR/MWh]",

ylab = "Density",

caption = "Data: ENTSO-E Transparency"

)

# Example 2 -------------------------------------------------------------------

main_frame %>%

plot_density(

x = value,

color = bidding_zone,

facet_var = bidding_zone,

facet_nrow = 1,

title = "Day-ahead Electricity Spot Price",

xlab = "[EUR/MWh]",

ylab = "Density",

caption = "Data: ENTSO-E Transparency"

)

The combined density plot highlights differences between bidding zones in the location and spread of prices. The faceted version provides a clearer view of each individual distribution.

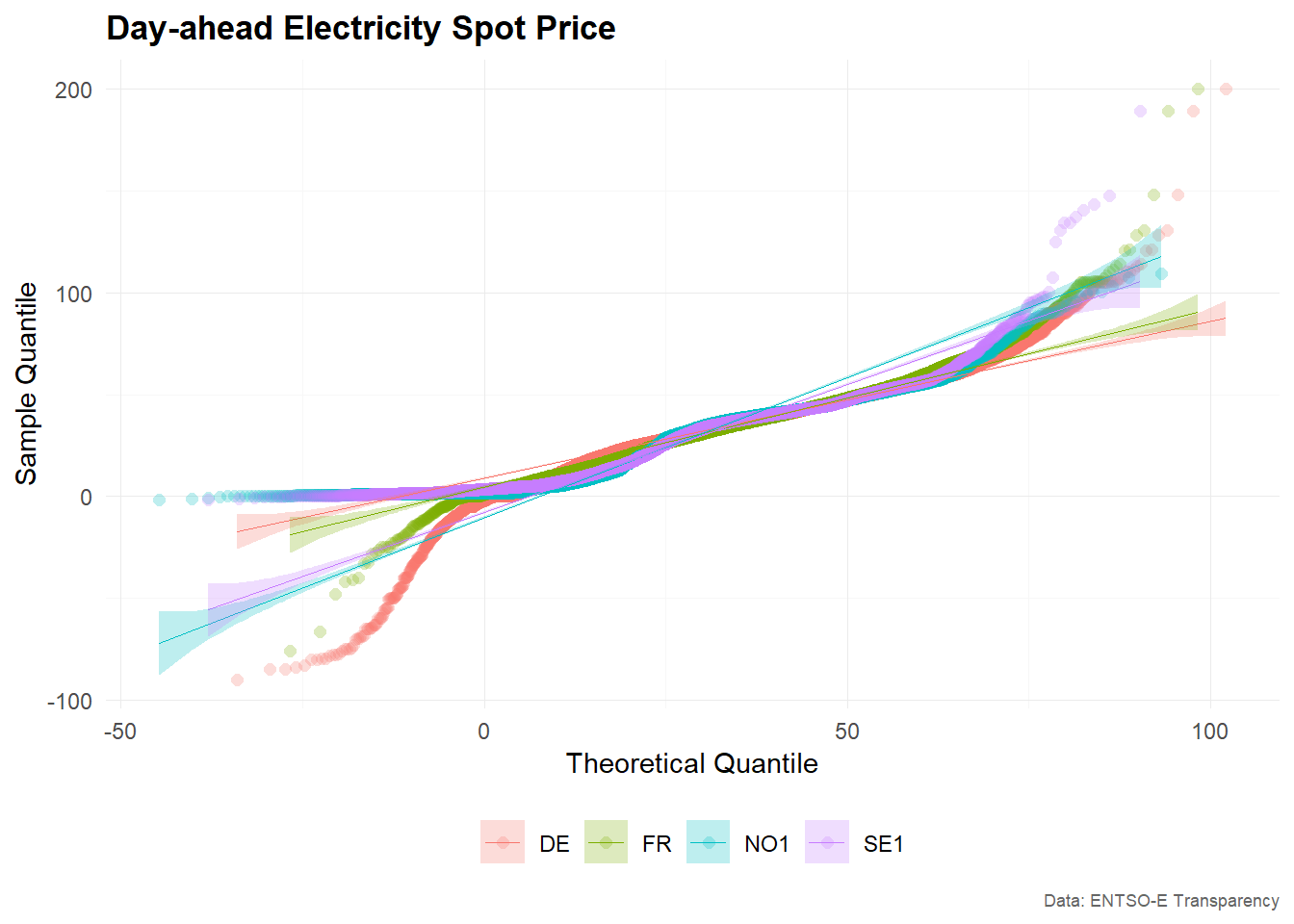

QQ-Plot

QQ-plots compare the empirical distribution of the observed values with a theoretical distribution, usually the normal distribution. They are useful for checking whether the data are approximately normally distributed.

For electricity prices, deviations from normality are common because prices can be skewed and may contain extreme values.

# Example 1 -------------------------------------------------------------------

main_frame %>%

plot_qq(

x = value,

color = bidding_zone,

title = "Day-ahead Electricity Spot Price",

xlab = "Theoretical Quantile",

ylab = "Sample Quantile",

caption = "Data: ENTSO-E Transparency"

)

# Example 2 -------------------------------------------------------------------

main_frame %>%

plot_qq(

x = value,

color = bidding_zone,

facet_var = bidding_zone,

title = "Day-ahead Electricity Spot Price",

xlab = "Theoretical Quantile",

ylab = "Sample Quantile",

caption = "Data: ENTSO-E Transparency"

)

If the observations were approximately normally distributed, the points in the QQ-plot would lie close to a straight line. Strong deviations from this pattern indicate skewness, heavy tails or outliers.

Summary

This vignette demonstrated several visualization functions from

tscv:

-

plot_line()for time series line charts -

plot_bar()for bar charts, here used to visualize partial autocorrelations -

plot_histogram()for histograms -

plot_density()for density plots -

plot_qq()for QQ-plots

Together, these plots provide a useful starting point for exploratory time series analysis. Line charts help inspect the temporal structure of the data, while distribution plots and correlograms help identify features that may be relevant for modelling and forecasting.